Debitum review 2025

Is Debitum a great platform for P2B lending? Find out in our Debitum review below:

Debitum

Pros:

Cons:

Review summary:

Debitum is probably the single best P2B lending platform for small business financing in Europe. On the platform, you can invest in pools of business loans that yield an average return of around 14.83% annually. The loans on the platform are protected with a 90-day buyback obligation, which means that your loans will be bought back by the broker in case the borrower can’t repay. Debitum is regulated and works under EU’s MiFID II which regulates off-exchange trading and requires continuous external auditing. Your funds are also protected up to €20,000 by the Investor Compensation Fund. This coupled with many excellent Trustpilot reviews makes Debitum one of the best P2B lending platforms right now.

It’s free to use the platform.

At P2PPlatforms.com, we strive to list only the absolute best companies in the P2P industry. Where appropriate, we also feature our partners. This doesn’t influence our evaluations. All opinions are our own.

Introduction to our Debitum review

Are you considering investing via the Debitum platform? Then read on. We’ve written this debitum.investments review to help investors determine if Debitum is the right choice for them.

Below you will find an overview of the things that we will discuss more in detail in this Debitum review. Simply click on the links to jump directly to the thing you want to know more about.

Learn about this in our Debitum review:

- What is Debitum?

- Key features

- Who can use Debitum?

- How safe is Debitum?

- Our experience with Debitum

- Debitum Investments Trustpilot rating

- Best Debitum alternatives

- Conclusion of our Debitum review

What is Debitum?

Debitum is a Peer-to-Business (P2B) lending platform focused on small business financing. You can use it to invest in pools of business loans from several business loan originators (brokers) from the UK, Estonia, and Latvia.

Debitum is a licensed investment brokerage company and is supervised by the Central Bank of Latvia. It is working under MiFID II which regulates off-exchange trading. Debitum is undergoing multiple external audits to maintain this regulation standard. On Debitum your funds are also protected up to €20,000 by the Investor Compensation Scheme by the Republic of Latvia.

The loans on the platform are secured by the Debitum buyback guarantee – a key platform feature that will be explained later in this review.

Check out this short explainer video from Debitum:

Debitum was launched in September 2018 by Martins Liberts, and the P2B platform has continued to grow ever since.

Currently, there are over 12,959 registered investors who have trusted the platform with over €83,230,000 in combined money deposits. The average return is around 14.83% annually.

With as little as €10, you can open an account and start investing at https://debitum.investments/.

Debitum statistics:

| Founded: | 2018 |

| Loan Type: | Business |

| Loan Period: | 3 – 48 Months |

| Loans Funded: | € 83,230,000 + |

| Debitum Users: | 12,959 + |

| Minimum Investment: | € 10 |

| Maximum Investment: | Unlimited |

| Debitum Interest Rate: | 14.83% |

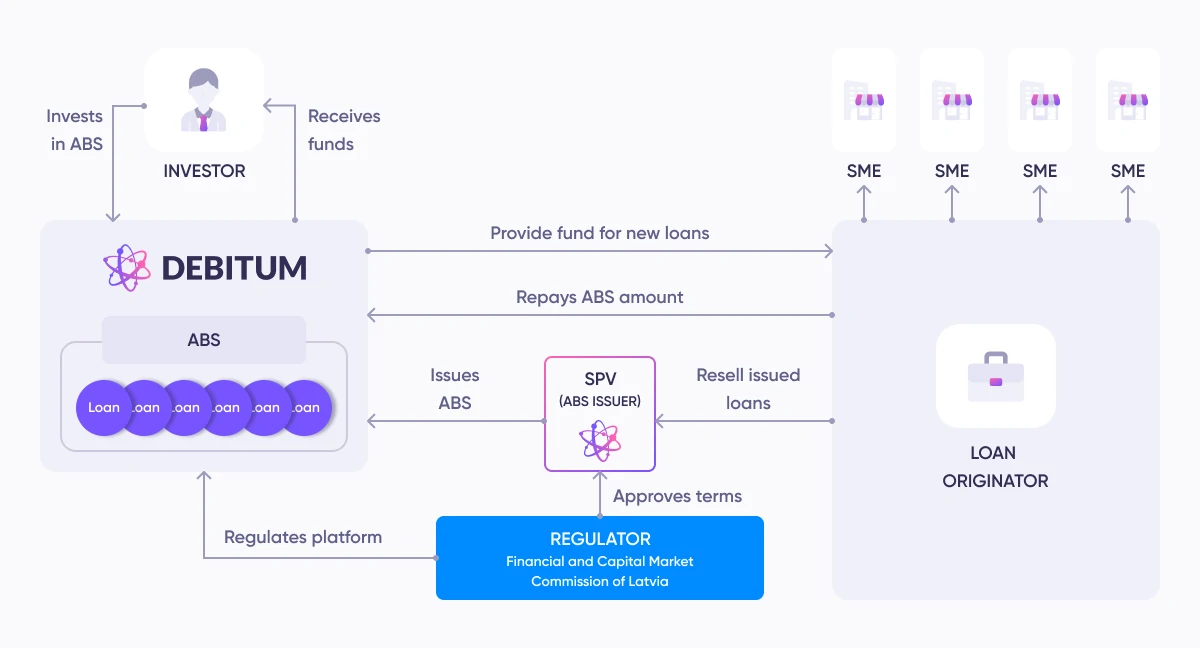

How Debitum works:

Debitum has a two-sided business model. On the one hand, they have investors (you). On the other hand, they have a range of loan originators (brokers) who are seeking funds for their borrowers.

Of course, you won’t get the full profit as the loan is not listed at the rate that the loan originator provides them. But you can still make a fair return from the investments.

When you have invested in a loan, the broker now has more liquidity to issue more loans.

The process is:

- A business goes to a broker to get a loan

- If the loan is accepted, the business gets the loan

- Several loans are converted into pools which are called asset-backed securities

- The asset-backed securities are now made available for investment on Debitum

- You can now invest in the loan and earn a profit

This is illustrated below:

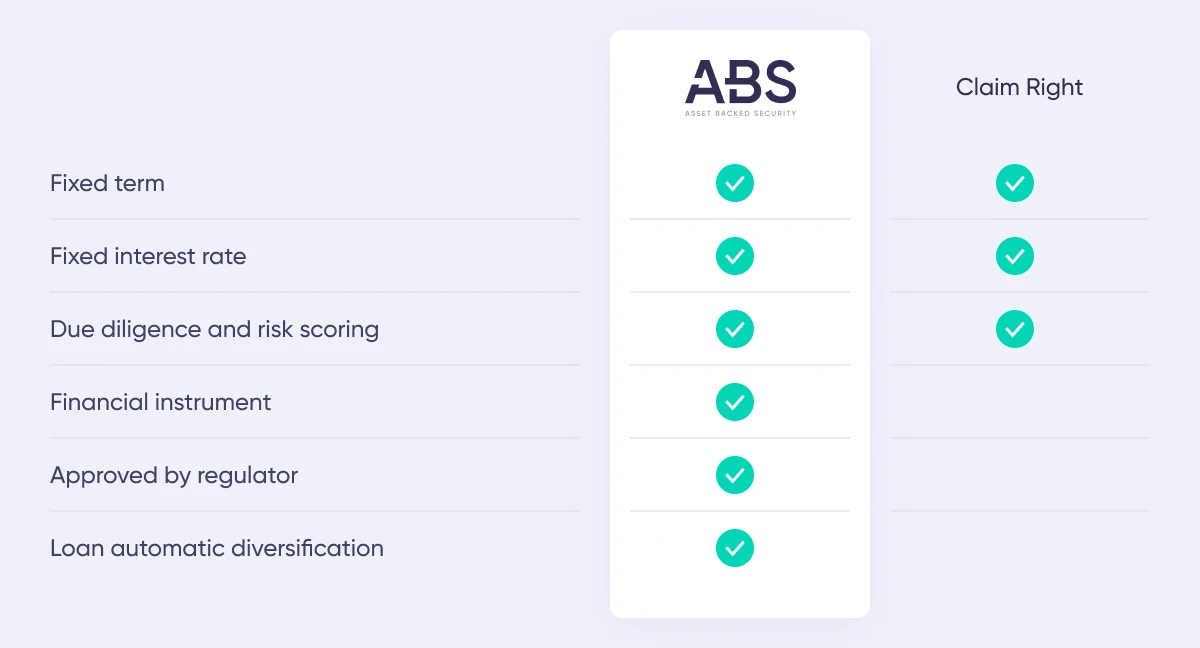

ABS (Asset-Backed Securities) are pools of many loans. Below you can see how ABS compares to claim rights that many other platforms offer their users to invest in.

Frequently asked questions:

Key features

We have already taken a look at some of the reasons why Debitum has become a popular choice among investors. In the following, we take a closer look at some of the key features that make it easy to invest via the platform:

1. Debitum buyback obligation

Debitum has a buyback obligation on its loans.

In short, the Debitum buyback obligation helps to protect you against loan defaults. In case a loan is not repaid, then the broker must repurchase the loan from you as an investor.

However, it is important to remember that a buyback guarantee is only as secure as the ones behind them – which in Debitum’s case would be the loan brokers. So if you decide to invest via Debitum, it’s a good idea to diversify between loans from several loan brokers.

You should also keep in mind that a buyback obligation acts as a form of insurance. Therefore, loans with a buyback obligation typically have a lower return than loans without a buyback obligation.

The buyback obligation has only been triggered on 1-2% of the loans on Debitum which is very low compared to other P2P lending platforms. The default rate remains at 0%.

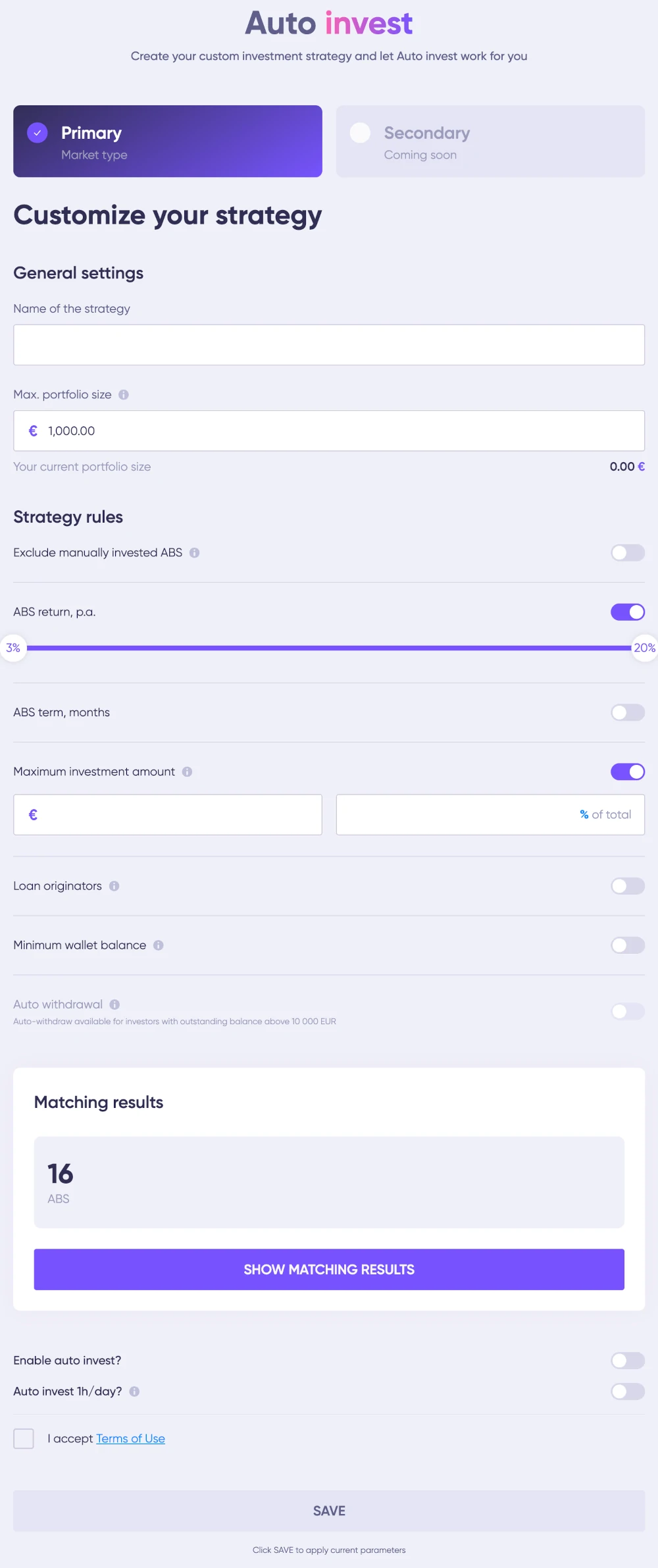

2. Debitum auto-invest

Another key feature that must be mentioned in this Debitum review is auto-invest. This feature allows investors to automatically invest in loans that fit certain criteria, which makes the investment experience a lot more pleasant. The Debitum auto-invest feature can do all you’d expect it to do.

To use a Debitum auto-invest plan, follow this guide:

- Make sure you have signed up

- Log in to your account

- Click “auto-invest” in the navigation

- Create a new auto-invest plan

Investors can customize their auto-invest strategy with precision, controlling variables such as:

- Maximum portfolio size dedicated to auto-investing

- The desired rate of return range

- Specific investment period

- Cap on single investment amount

- Option to include or exclude certain loan originators

- Setting a minimum wallet balance to ensure funds are available for withdrawal or manual investment

What sets Debitum’s auto-invest tool apart from other platforms is the auto-withdrawal feature, which is available for portfolios over €10,000. This allows investors to automatically transfer the monthly interest earned into their bank account, eliminating the need for manual intervention. The reason auto-invest is not available to smaller portfolios could be that fees between banks can eat too much into your profits for small monthly payments.

3. Debitum sign-up bonus

Debitum is offering a cashback bonus of 1% for new investors who sign up from affiliates. If you decide to invest via the debitum.investments, you can click the button below to get the + 1% sign-up bonus:

Who can use Debitum?

Both individuals and companies can invest via Debitum.

Individuals

If you want to invest as an individual, you must at least meet the following requirements:

- Being at least 18 years old

- Having a bank with AML/CFT equivalent to the EU

- Getting your identity verified by Debitum

- Getting your address verified by Debitum

If you match these requirements, you can start investing via the platform.

Companies

Whether you run a company, investing via Debitum is also possible.

There is some further information and details that you will have to provide Debitum if you want to use the platform as a company. You can learn about these on the website.

Available countries

Debitum is a globally available P2B lending platform. However, some countries might be restricted due to special financial regulations.

Sign up tutorial

In the following tutorial, you can learn how to sign up and use the P2B lending platform at https://debitum.investments/.

How safe is Debitum?

To determine if Debitum is safe, we have taken a look at some of the potential upsides and downsides of investing with Debitum.

When you consider the safety of Debitum, we don’t recommend that you rely solely on information found in our Debitum review as this is only based on our research. We always recommend that you also do your research before investing any money.

In the following part of our Debitum review, you can read an analysis of some of the main risks of using Debitum, along with the mitigation strategies employed by the platform:

Loan default risk

Loan default risk is the possibility that borrowers will fail to meet the obligations of loan repayment. This is a common risk in P2P lending, where individual or business borrowers may default due to various reasons, including financial distress or poor creditworthiness.

Loan default risk mitigation strategies by Debitum:

- Solid collateral: Debitum secures all investments with easily convertible collateral, such as commercial pledges, mortgages, and receivables from invoices. This collateral can be utilized to recover funds in the event of a default.

- Late penalties: Debitum imposes severe penalties of 10-20% per annum on loan originators for late payments and incentivizes timely repayments, thereby reducing the default risk.

- 90-day buyback obligation: If the assets on Debitum are not repaid to the investor after a combined grace and penalty period of a maximum of 90 days, the loan originator must repay the loan or replace it with a similar risk-class asset. This significantly reduces the risk for investors as the loan originator assumes responsibility for defaults.

In general, the best way to hedge against loan default risk is to invest in many different loans. This is done automatically on Debitum, as you are investing in asset-backed securities.

Loan originators risk

The loan originator risk involves the loan originator facing financial difficulties or failing to adhere to agreed standards, which could impact their ability to meet the buy-back obligations. This could be due to poor management or a lack of control of finances which could lead to bankruptcy like any other business.

Debitum’s loan originators:

- Trible Dragon

- Flexidea

- Evergreen Capital

- DN Funding Alpha

- Sandbox Funding

Debitum has a lot of different loan originators to choose from on the platform which makes it possible to lower the specific loan originator risk by investing via multiple loan originators.

Loan originator risk mitigation strategies by Debitum:

- 4-step due diligence process: The comprehensive due diligence process, including onboarding checks, credit scoring, and regular monitoring, minimizes the risk associated with loan originators by ensuring they are credible and financially stable.

- 10-30% skin in the game: Debitum requires loan originators to retain a share of each loan of 10%-30%, which ensures they have a vested interest in the quality and performance of the loans, thereby aligning their interests with the investors.

Debitum bankruptcy risk

The risk of bankruptcy is an important consideration for any investment platform, including P2P lending platforms like Debitum. Bankruptcy of a P2P lending platform can potentially jeopardize investor funds and access to their investments.

SIA DN Operator, the company behind Debitum, made a small loss in 2022, as stated in its annual report for 2022. This might add a bit of risk as the likelihood of bankruptcy occurring is lower for profitable P2P lending platforms.

Overview of the historic net profit/loss for Debitum:

- 2020: Net loss of €3,134

- 2021: Net loss of €83,693

- 2022: Net loss of €110,487

When assessing the overall profit/loss of a company it is important to keep in mind that many companies use a lot of capital in the beginning on expenses that can make the company grow. Even though Debitum is not profitable, they have some decent risk mitigation strategies in place.

Bankruptcy risk mitigation strategies by Debitum:

- Regulatory compliance and licensing: Being a licensed entity under stringent regulatory oversight (Central Bank of Latvia and MiFID II) adds a layer of security and ensures that Debitum operates with financial prudence.

- €20,000 insolvency protection: In the unlikely case of Debitum’s insolvency, there is a protection of up to €20,000 per investor, safeguarding against total loss.

- Separated accounts for investor funds: Debitum keeps investor funds separate from Debitum’s operational funds ensuring that in the event of bankruptcy, these funds are not accessible to creditors.

If Debitum goes bankrupt, the investors can according to the loan agreements approach loan originators directly and they would provide all owed funds directly to the investor.

Financial turndown risk

As P2P investing is a newer thing in the investment world, it can be difficult to predict how a financial turndown would affect this form of investment. As a starting point, it is, therefore, a really bad idea to invest your entire investment portfolio in P2P investments.

Therefore, many investors also diversify into more traditional forms of investment such as equities, bonds, and real estate.

Since investing is an individual thing, we do not know what will be best for you. But if you put together your investment portfolio, make sure that it reflects your knowledge of the investments in it, as well as your risk appetite. If in doubt about how to do so, make sure to seek help from a professional investment planner.

Is Debitum safe?

So far, Debitum has proved to be a more safe alternative to other P2P lending platforms.

The platform has a 0% default rate and only a very small amount of loans are bought from investors with the buyback guarantee.

At the same time, Debitum was one of the platforms that kept doing well during the COVID-19 shock, while other platforms struggled a bit.

This indicates that the Debitum is doing a good job at picking loan originators and loans for the marketplace.

At the same, Debitum has also made measures against its bankruptcy. With these things in mind, we believe that Debitum is among the safer platforms on the market.

However, other factors, such as a lack of knowledge about how a financial turndown will affect the P2P lending industry, are also risk factors worth considering.

In conclusion, while risks in P2P lending like loan defaults, loan originator issues, and platform bankruptcy are inherent, Debitum has instituted several robust measures to mitigate these risks. The platform’s approach combines regulatory compliance, financial safeguards, and stringent due diligence to create a secure environment for investors.

Our experience with Debitum

Our experience with Debitum has been very positive. Right from the outset, the sign-up process on Debitum was notably straightforward and user-oriented. The platform’s interface is designed with intuitiveness in mind, making navigation and investment decisions seamless and hassle-free. This ease of use is especially beneficial for newcomers to P2P investing.

A key highlight in our experience was Debitum’s robust performance during challenging times, such as the COVID-19 pandemic. Unlike several competing platforms, Debitum managed to shield investor returns from the adverse impacts typically seen during such global crises. This resilience is indicative of the platform’s strong risk management strategies and prudent operational approach.

Our continued positive experience with Debitum has been underpinned by its stability and reliability. The platform’s consistent performance and the absence of negative surprises have fostered a sense of trust and confidence in our investment journey.

This is among the reasons why we gave the platform a very good rating in this Debitum review.

A slight negative thing about the platform has been that the auto-invest feature was unavailable for a long period when the platform had to be regulated. This is no longer an issue as the regulation process is over. It is also worth noting that the return on Debitum has been a bit volatile over the years ranging at 9-15%. This is a bit high compared to other platforms.

Below you can see a screenshot taken from our account at Debitum:

As you can see we have achieved an all-time interest rate of 9.72%. This is a result that we find attractive since there are only a few loans going bad on the platform compared to some of the competitors.

Debitum Investments Trustpilot rating

Debitum Investments has an average TrustScore of 3.5/5 based on 59 reviews on Trustpilot, which is a reasonable rating compared to other platforms. Investors appreciate its regulated status, timely interest payments, and generally supportive customer service. Some concerns revolve around delayed repayments on Ukrainian loans, lengthy verification processes, and the lack of a secondary market for liquidity.

Best Debitum alternatives

Not sure Debitum is the right choice for you after reading our Debitum review? Then there are also some good Debitum alternatives to consider. The following are some of our favorites:

- PeerBerry (highly rated consumer lending platform)

- ReInvest24 (highly rated real estate crowdfunding platform)

- Mintos (largest P2P lending platform in Europe)

Even if you use the Debitum P2P lending platform, it might be a good idea to take a closer look at some of the above platforms. By using multiple platforms, you can reduce your platform risk and diversify your portfolio further.

In the following, you can learn more about how Debitum compares to near competitors that many investors ask about:

Mintos vs Debitum

The most frequently asked-about comparison is Mintos vs Debitum. The main difference between the two platforms is their focus.

Mintos is a P2P lending platform that makes it easy for investors to diversify between a lot of different loan types including payday loans, agricultural loans, business loans, car loans, and more.

Debitum is a platform that focuses only on small business financing. The platform has a focus on making the experience very safe with thorough due diligence and buyback obligations on investments.

Conclusion of our Debitum review

Debitum stands out as a top choice in the world of P2B lending, thanks to its impressive balance of safety and returns. It might even be the single best P2B lending platform in Europe right now depending on your risk profile and preferences.

Debitum currently has a default rate of 0% and only 1,42% of loans have triggered the buyback obligation of the platform since 2018. This indicates that Debitum has a good due diligence process and that the risk compared to other platforms is fairly low. Further emphasizing its robust risk management, Debitum didn’t experience some of the negative impacts on investor returns that happened on some competing platforms during COVID-19.

Regarding safety, Debitum stands out as a licensed investment brokerage firm, under the vigilant supervision of the Central Bank of Latvia. Operating in compliance with MiFID II, a directive that governs off-exchange trading activities, Debitum adheres to stringent regulatory standards. This compliance is continuously validated through numerous external audits, ensuring that the platform consistently meets the high regulatory requirements set by MiFID II. Investor funds are protected by up to €20,000 through the Investor Compensation Scheme.

When it comes to returns, Debitum offers an average return of about 14.83%. This is an excellent average return, but it is worth noting that the return on Debitum has been more volatile than on some other platforms. Debitum is one of the platforms that most frequently have

In addition to the high average return on the platform, you will often find cashback bonuses of up to 5% for both new and existing users on the platform. This is not as common on other platforms as many platforms only offer cashback to incentivize users to sign up and not rewarding existing investors. The cashback bonuses are typically announced on Debitum’s homepage.

For those seeking a balance of attractive returns and robust security in the P2B lending arena, Debitum presents itself as a strong, dependable choice. Its meticulous approach to risk management, coupled with its regulatory compliance, makes it a standout platform, arguably one of the best in the current market.

Don’t just take our word for it – many users agree! Debitum has received lots of great reviews on Trustpilot, scoring way higher than many other P2P lending platforms. This high TrustScore is like a vote of confidence from its users.